Composition Scheme is a simple and easy scheme under GST for taxpayers. Small taxpayers can get rid of tedious GST formalities and pay GST at a fixed rate of turnover. This scheme can be opted by any taxpayer whose turnover is less than Rs. 1.0 crore*.

*CBIC has notified the increase to the threshold limit from Rs 1.0 Crore to Rs. 1.5 Crores.

Contents

1. Who can opt for Composition Scheme

A taxpayer whose turnover is below Rs 1.0 crore* can opt for Composition Scheme. In case of North-Eastern states and Himachal Pradesh, the limit is now Rs 75* lakh.

As per the CGST (Amendment) Act, 2018, a composition dealer can also supply services to an extent of ten percent of turnover, or Rs.5 lakhs, whichever is higher. This amendment will be applicable from the 1st of Feb, 2019. Further, GST Council in its 32nd meeting proposed an increase to this limit for service providers on 10th Jan 2019*.

Turnover of all businesses registered with the same PAN should be taken into consideration to calculate turnover.

*CBIC has notified the increase to the threshold limit from Rs 1.0 Crore to Rs. 1.5 Crores.

*Update as on 10th Jan 2019

As per 32nd GST Council Meeting held on 10th Jan 2019, Service Providers can opt into the Composition Tax Scheme, and the Government has set the threshold turnover for service providers at Rs. 50 lakhs to be eligible for this scheme.

2. Who cannot opt for Composition Scheme

The following people cannot opt for the scheme-

- Manufacturer of ice cream, pan masala, or tobacco

- A person making inter-state supplies

- A casual taxable person or a non-resident taxable person

- Businesses which supply goods through an e-commerce operator

3. What are the conditions for availing Composition Scheme?

The following conditions must be satisfied in order to opt for composition scheme:

- No Input Tax Credit can be claimed by a dealer opting for composition scheme

- The dealer cannot supply GST exempted goods

- The taxpayer has to pay tax at normal rates for transactions under the Reverse Charge Mechanism

- If a taxable person has different segments of businesses (such as textile, electronic accessories, groceries, etc.) under the same PAN, they must register all such businesses under the scheme collectively or opt out of the scheme.

- The taxpayer has to mention the words ‘composition taxable person’ on every notice or signboard displayed prominently at their place of business.

- The taxpayer has to mention the words ‘composition taxable person’ on every bill of supply issued by him.

- As per the CGST (Amendment) Act, 2018, a manufacturer or trader can now also supply services to an extent of ten percent of turnover, or Rs.5 lakhs, whichever is higher. This amendment will be applicable from the 1st of Feb, 2019.

4. How can a taxpayer opt for composition scheme?

To opt for composition scheme a taxpayer has to file GST CMP-02 with the government. This can be done online by logging into the GST Portal.

This intimation should be given at the beginning of every Financial Year by a dealer wanting to opt for Composition Scheme.

Here is a step by step Guide to File CMP-02 on GST Portal.

5. How Should a Composition Dealer raise bill?

A composition dealer cannot issue a tax invoice. This is because a composition dealer cannot charge tax from their customers. They need to pay tax out of their own pocket.

Hence, the dealer has to issue a Bill of Supply.

The dealer should also mention “composition taxable person, not eligible to collect tax on supplies” at the top of the Bill of Supply.

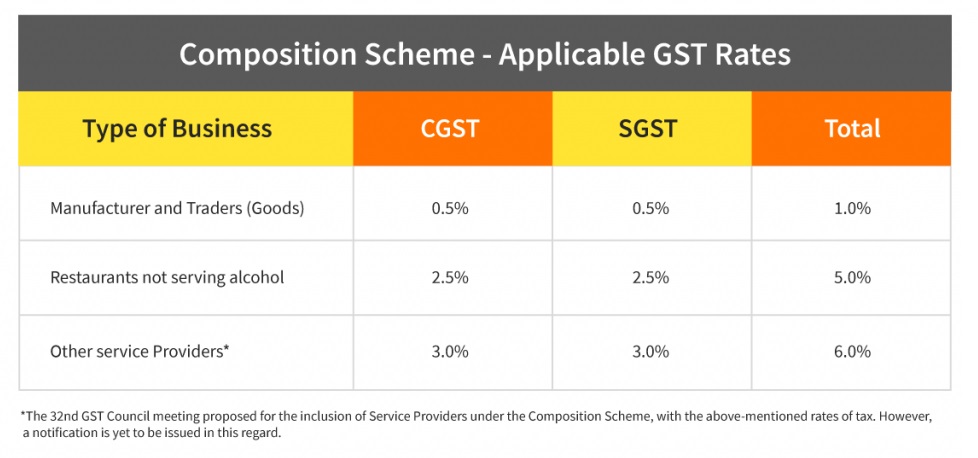

6. What are the GST rates for a composition dealer?

Following chart explains the rate of tax on turnover applicable for composition dealers :

As per notification dated 01.01.2018, turnover in case of traders has been defined as ‘ Turnover of taxable supplies of goods’.

7. How should GST payment be made by a composition dealer?

GST Payment has to be made out of pocket for the supplies made.

The GST payment to be made by a composition dealer comprises of the following:

- GST on supplies made.

- Tax on reverse charge

- Tax on purchase from an unregistered dealer*

*Only on the specified categories of goods and services and well as the notified class of registered persons with effect from 1st Feb 2019 but is yet to be notified. Hence, not applicable until then.

8. What are the returns to be filed by a composition dealer?

A dealer is required to file a quarterly return GSTR-4 by 18th of the month after the end of the quarter. Also, an annual return GSTR-9A has to be filed by 31st December of next financial year*.*Update as on 22nd December 2018: Due date for filing GSTR-9, GSTR-9A and GSTR-9C is extended till 30th June 2019 by CBIC for FY 2017-18

Latest update on Due dates:

Due date for GSTR-4 for the period Oct-Dec 2018 is 18.01.2019

Also, note that a dealer registered under composition scheme is not required to maintain detailed records.

9. What are the advantages of Composition Scheme?

The following are the advantagesof registering under composition scheme:

- Lesser compliance (returns, maintaining books of record, issuance of invoices)

- Limited tax liability

- High liquidity as taxes are at a lower rate

10. What are the disadvantages of Composition Scheme?

Let us now see the disadvantagesof registering under GST composition scheme:

- A limited territory of business. The dealer is barred from carrying out inter-state transactions

- No Input Tax Credit available to composition dealers

- The taxpayer will not be eligible to supply exempt goods or goods through an e-commerce portal.

![]()